22. desember 2020

Nbims aksjeplukkingsvirksomhet taper to milliarder kroner per år. Offentligheten, politikere og Finansdepartementet bør reagere.

22. desember 2020

Nbims aksjeplukkingsvirksomhet taper to milliarder kroner per år. Offentligheten, politikere og Finansdepartementet bør reagere.

16. desember 2020

Vi trenger en åpen, opplyst og ærlig

diskusjon om Oljefondets prestasjoner.

Men da kan vi ikke se bort fra

kostnader og risiko, slik oljefondssjefen

gjør.

(Foto: Fartein Rudjord)

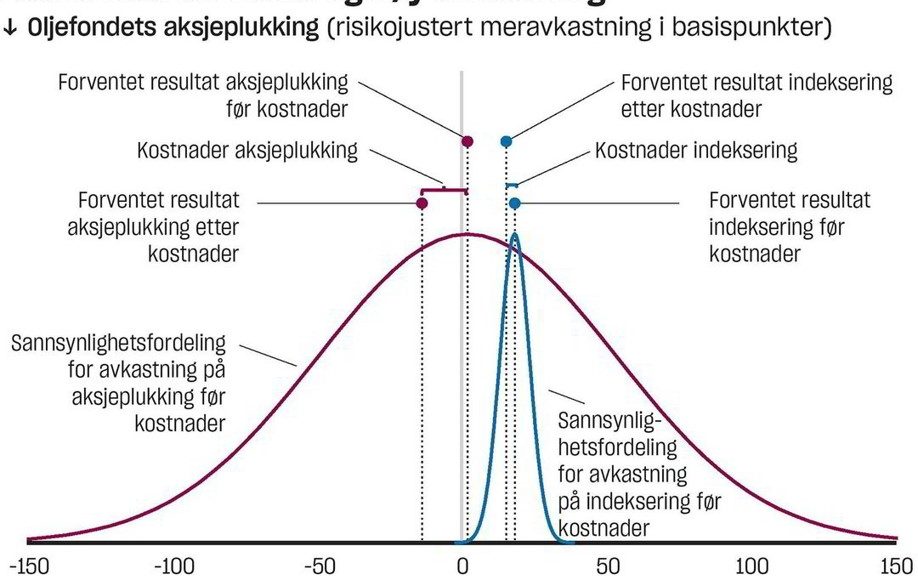

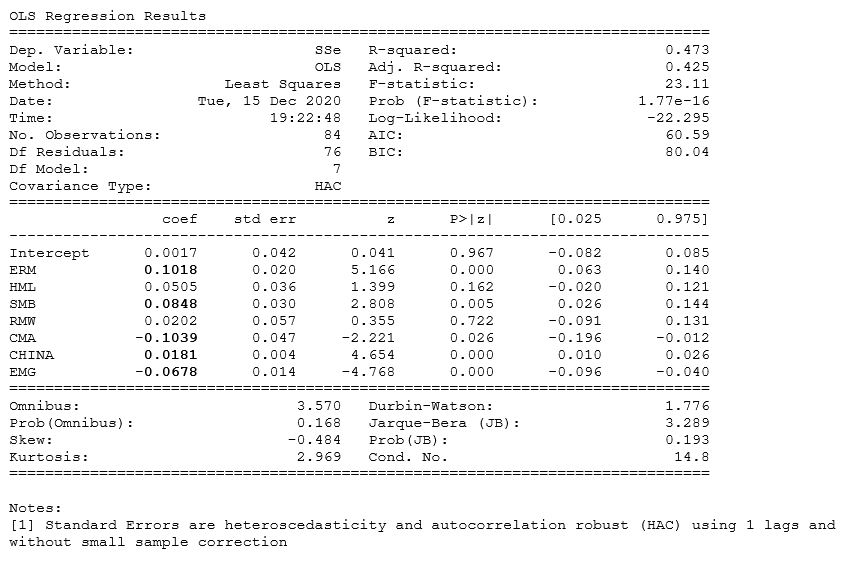

We show that with updated data covering the period 2013-2019, the risk adjusted return before costs from the stock picking-activity in the Government Pension Fund Global (GPFG) is zero for all practical purposes, and thus not significantly different from zero. The costs of managing this part of the portfolio appears to amount to about 20 bp per annum. After costs the return is thus negative

For explanation on methodology and factors, please see previous editions of this exercise.

Sources:

Underlying data:

201215_data

9. desember 2020

Det er en misforståelse at bobler eksisterer

i kapitalmarkedet og at aktive

forvaltere styrer klar av dem.