A report on NBIM’s performance on real estate. Photo: Stian Lysberg Solum/NTB

The article and the op-ed:

A report on NBIM’s performance on real estate. Photo: Stian Lysberg Solum/NTB

The article and the op-ed:

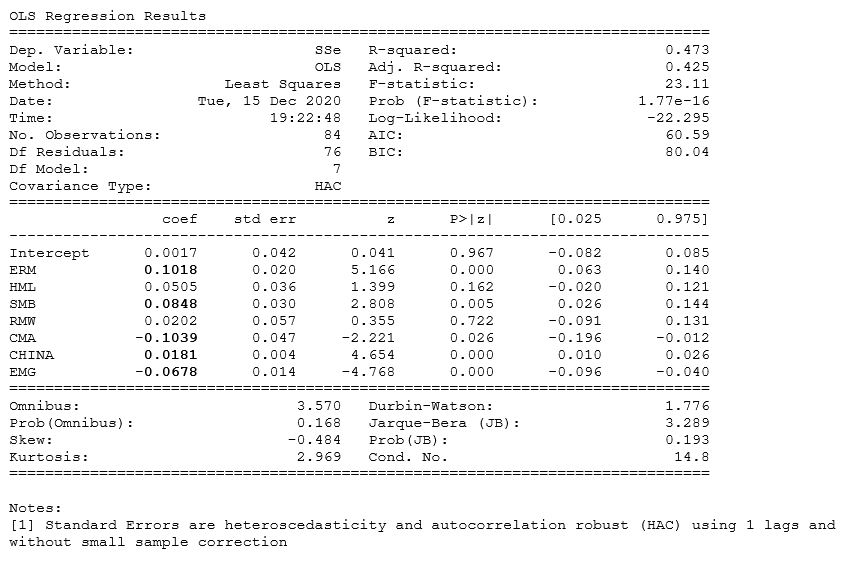

We show that with updated data covering the period 2013-2019, the risk adjusted return before costs from the stock picking-activity in the Government Pension Fund Global (GPFG) is zero for all practical purposes, and thus not significantly different from zero. The costs of managing this part of the portfolio appears to amount to about 20 bp per annum. After costs the return is thus negative

For explanation on methodology and factors, please see previous editions of this exercise.

Sources:

Underlying data:

201215_data

28 August 2019

We show that with updated data covering the period 2013-2018, the risk adjusted return before costs from the stock picking-activity in the Government Pension Fund Global (GPFG) is negative, and not significantly different from zero. The costs of managing this part of the portfolio appears to amount to about 20 bp per annum. After costs the return is thus negative.

4 April 2018

Given that the costs of stock-picking within the GPFG are substantial and this produces at best a zero additional return and at worst loses money before costs, it is difficult to understand why the Ministry of Finance on behalf of the Norwegian public would continue to ask NBIM to use resources to finance this activity.

180404_Risk adjusted performance of the stock picking in the GPFG

Fagnotat om fastsettelse av garantipremie.